deutsche Fassung

Version en español

Русская версия

Version française

2.1. System

The bookkeeping according to the description of the year 1494 represents mainly the production factor capital; the factor labor is only taken into account with the personnel costs. It is

differentiated according to the origin of the capital. Equity is attributable to the entrepreneur or the shareholders. It may consist of deposits or retained earnings. Also the current profit or

loss belongs to the equity. Debt capital belongs to persons who are not among the co-entrepreneurs. They are entitled to repayment and often receive interest.

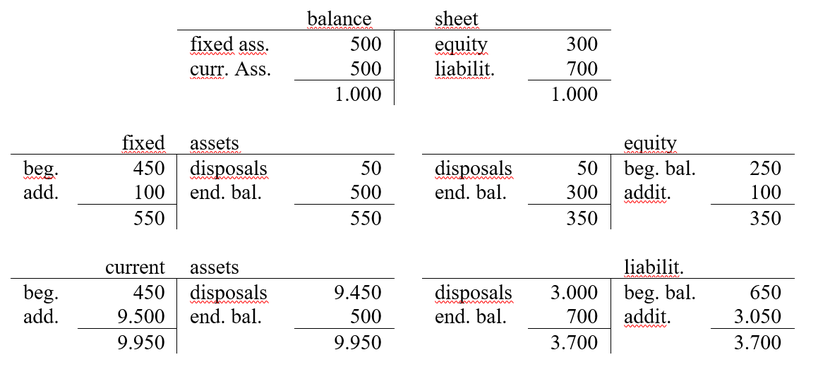

The capital is used in the company for potential factors and repeating factors. According to this classification, the use of capital is divided into fixed assets and current assets. The sums of

wealth (use) and capital (origin) are equal in amount. They are contrasted in a balance (balance = equilibrium), with the left side (called assets) representing the assets and the right side

(called liabilities) the capital.

The balance sheet is then broken down into accounts, where entries and exits are recorded.

Fig. 3: Accounts and balance sheet

(Source: own representation)

The final balance transferred to the balance sheet was called the "balance".

The accounts can be broken down into subaccounts again. For clarity, it is necessary to combine several accounts into one balance sheet item. Then, in the 1494 system, each balance sheet item

would have to be treated like an account and each account as a subaccount.

The balance sheet is set up at a time. The operational activity takes place however in periods. This is especially true for the gain or loss resulting from the difference in income and expense of

a period. It is part of the equity. To record this size in the balance sheet, the Accounting 1.0 of 1494 creates a profit and loss account as a sub-account of equity. This is subdivided into

sub-sub-accounts, in which income and expenses are recognized in different ways.

For the accounts, a distinction is not made between assets and liabilities, but between debit (left) and credit (right). The accounts themselves are divided into balance sheet accounts that are

included in the balance sheet and income statement accounts. Stock accounts are divided into asset accounts and liability accounts for the capital items. Success accounts are separated into

expense and income accounts. For asset accounts, additions to assets are posted in debits and outflows in credit. In the case of the liability accounts, conversely, the additions to the capital

in the credit and the outflows in the debit are recorded. Income accounts include the income and the expected income corrections. In the case of expense accounts, the expense is posted to the

debit and expense adjustments in credit.

Each business transaction has two sides. The purchase of an item (payment later) increases the assets (debit) and at the same time the debts (credit) increase. If this item is paid later, the

debt (debit) and at the same time the money stock (credit) decreases. The balance of the balance sheet is maintained if each transaction is recorded on both sides and the sums of debits and

credits are always identical.

In addition to double entry and deferred accounting, each business transaction in the 1494 system is recorded twice, in chronological order in journals and factually in accounts. A further

explanation of the term "double entry accounting" is the possibility to determine the profit in two ways, namely by the so-called business asset comparison on the comparison of the equity at the

beginning and end of the period, which is determined from the difference of assets and debts ; and the income statement based on the income and expense accounts.

All bookings are based on receipts. Here, a distinction must be made between internal and external documents. Another distinction is whether they depict external events or internal events.

External documents, which are thus created by non-company members, have the higher evidential value. By their very nature, however, they can almost exclusively relate to events with external

effects, in which case the company does business in the procurement or sales market. However, documents about internal processes cannot normally be made by external companies. An exception could

be e.g. be a notarised deed on a change in the ownership structure. Self-documents with external effect are e.g. Invoice copies of services rendered. With self-prepared-documents about internal

processes, there can be gaps. This group includes e.g. Logs from production about the type and number of finished products. But there are also processes in which there is no awareness of the

balance sheet relevance.

In the bookings, reference must be made to the respective document by means of a document number. With these references, the background of the booking can be clarified quickly if necessary.

2.2. Journals

The chronological recording of business transactions in journals takes place using posting records, that is, the data required for further processing. In the textbooks, this is reduced to the

statement of accounts and amounts. In practice, however, also in the system of 1494 document type, document no. and document date as well as a short text. For the accounts, a distinction is made

between the accounts with debit and credit postings. A short form of the booking record is then displayed "per [debit-account] to [credit-account]", whereby there may be several accounts on both

sides. One speaks also of "debit" [debit account] and "credit" [have-account]. After registering an operation in the journal, the posting record was then transferred to the accounts that were

kept as index cards. In the early days, single sheets were used, which were bound to a book after the end of the year and the preparation of the balance sheet.

In the 20th century, the strict chronology was softened and different journals were kept for frequent transactions such as sales, purchases of goods or payments. This made it possible to record

the transactions only on the ledger accounts and to transfer only the totals of the journal page to the nominal accounts and to refer to this page. The payment date was later noted in a free

column in the journal to get an overview of outstanding items.

An extension of this technique is the "American Journal". Here, all business incidents were only presented in the journals and mapped to different columns that replaced the accounts. Debits and

credits were often replaced by plus and minus, which halved the required number of columns (or avoided doubling). This required a manageable number of accounts or columns. Business with customers

and suppliers was recorded together in one column. The open items were kept in an orderly document storage, in which the unpaid and afterwards the paid invoices were filed in front of a cover

sheet. The filing was arranged alphabetically according to the names of the customers or suppliers. On personal accounts could be waived so.

The American Journal was normally started monthly with new leaves. The figures of the individual months were transferred to an annual overview. From these annual overviews it was possible to

quickly create balance sheets and profit and loss statements for individual months or the year in which they occurred. They were not very profound, though. Depreciation and other valuation issues

also had to be taken into account in secondary calculations.

2.3. Nominal Accounts and Charts of Accounts

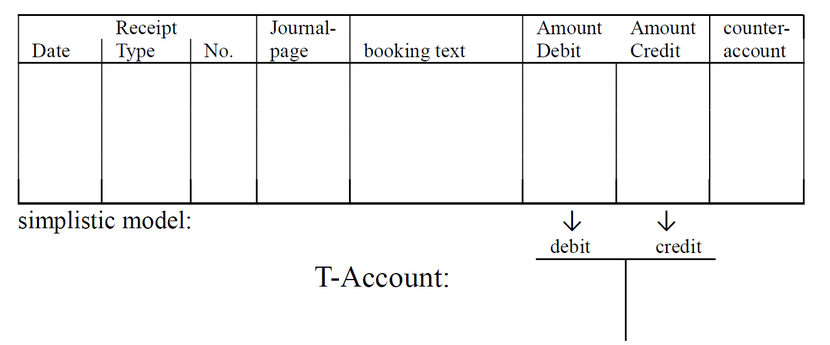

In the system of 1494, accounts are the settlement unit for the itemized business transactions. Their purpose was to be completed on the balance sheet, G.u.V account or other accounts. After

that, they were zeroed. In them one could read only the development of the amounts. In the textbooks the accounts are presented in a simplistic model as a "T-Account"; a large part of the account

data is omitted.

Fig. 4: Nominal Account and T-Account

(Source: own representation)

This simplification cannot be criticized because the additional data are of no importance for the presentation of the accounting system. The task of a model, to explain simplistic, is thus

fulfilled with the T-account.

Because of the large number of accounts, it is necessary to uniquely identify the accounts with an account number and to structure them meaningfully in charts of accounts. There are different

principles and suggestions for this. 1937 was in the decree of the Imperial and Prussian Minister of Economic Affairs and the Imperial Commissioner for Pricing v. 11.11.37 - II 19263/37 VI

9991/37 concerning the guidelines for the organization of accounting (as part of a single accounting system) a chart of accounts is mandatory. It followed the so-called process structure

principle and had the following account classes for the first position of the account numbers:

Fig. 5: Account classes of the 1937 remittance account

0 Dormant accounts or investment and capital accounts

1 financial accounts

2 delineation cones

3 accounts of raw materials and supplies or goods purchase accounts

4 accounts of cost elements

5 clearing accounts when using a Overhead allocation sheet

6 accounts for cost accounting in conjunction with the free class 5

7 accounts of semi-finished and finished products

8 Revenue Accounts

9 closing accounts

(Source: own representation)

Although the accounting framework has not been mandatory since 1953, the process structure principle has remained in many companies to this day. In addition, the

Annual-Accounts-Classification-Principle is relevant, which numbers the accounts according to their arrangement in the items of the annual financial statements.

2.4. closing accounts

The 1494 system, in principle, does not allow for monthly or quarterly financial statements. Since the accounts are closed via the income statement or the balance sheet, they cannot be rebooked

afterwards, because the accounts had to be closed before. Both analyses were presented in the form of an account, whereby all balance sheet accounts with debit surplus (balance in credit) had to

be shown on the assets side and those with credit surplus (balance in debit) in on the liabilities side. Success accounts with credit overhang (balance in debit) were shown on the right side of

the income page and those with debit overhang (balance in credit) on the expense side. Adjustments with balances on the "wrong page" had to be completed beforehand via another account.

It could also be created by this system, no trial-proof conclusion. If you find errors after installation, a correction is complicated. The closure of the failed account must be cancelled (=

repeat faulty posting with reverse debit-credit assignment and thereby cancel). Then the correct value has to be determined. Because a mistake in the double-entry accounting results in at least

one more error in the contra account, the same correction must be made there as well. However, there can also be further consequential errors with multiple correction requirements. For many

detected errors with their follow-up errors, the entire closing postings are very confusing.

To limit such difficulties, the main financial statements were developed. Here all accounts were listed before their closing with the sum of debit and credit entries and the resulting debit or

credit overhang. The debit / credit overhang has been allocated to different columns of assets, liabilities, income or expense. From this, preliminary balance sheet and P/L-drafts were prepared

and then examined for conclusiveness and possible errors. In the case of errors, correction columns were added in which the necessary corrections with plus and minus were entered. After that new

designs could be created. The goal was to recognize all forgotten bookings and discover any errors before closing the accounts. With a quarterly summary of financial statements, unofficial

quarterly financial statements could also be prepared.

In addition, the traditional US-American balance sheets should be mentioned, which did not represent an account, but a tabular equity calculation in staggered form. They followed the basic

pattern:

Fig. 6: Traditional balance sheet structure in the USA before 1934

money holdings

+ Customer demands

+ Supplies

– Supplier liabilities

= Working capital

+ Other assets

– Other debts

= Equity

(Source: own illustration)

Here there was no transfer of accounts to the balance sheets. The bookkeeping was rather understood as a database, from which the evaluations were created. Whether this database consisted of

accounts or American journals was irrelevant.