deutsche Fassung

Version en español

Русская версия

1. History of Accounting

Probably the invention of the characters was a step towards the development of an accountancy. People wanted to have an overview of their supplies.

The bookkeeping is therefore very old, even if this chapter does not go back to the early history of mankind.

1.1. Paccioli

There is evidence that the emergence of accounting is closely related to the development of characters. Early records often deal with production and storage quantities of agricultural products.

Maybe the script was just invented to build an accounting department. It would not have been possible without a character.

Italian merchants developed the double-entry system in the 14th century. Government accounts of Genoa, dating from 1340, containing government receipts and expenditures, as well as all tax, bond,

and penalties, clearly show double entry bookkeeping. (Federal Association of Accountants and Controllers e.V., https://www.bvbc.de/baden-wuerttemberg/chronik/geschichte-der-buchhaltung /)

Indirect references to their existence are even dated to 1310. It uses the Arabic numbers instead of the Roman ones and also records every transaction twice, not just once, once on the debit side

and once on the credit side.

Luca Pacioli described this method in 1494 in a printed book as a Venetian bookkeeping - and spread it as a new standard from Italy throughout Europe. His book "Summa de arithmetica, geometria,

proportioni et proportionita", written in Latin, deals only with one chapter of the Venetian bookkeeping and otherwise deals with the system of Arabic numbers that reached Europe via the

commercial contacts of the Republic of Venice. For the first time since 1511, a record has been handed down from Germany using the double-entry method - by the accountant of the Fugger trading

house, Matthäus Schwarz. The Arabic numbers were comprehensively explained in German in 1524 with the book "Rechnung auff der Linihen und Federn" by Adam Ries (or Riese). In the 16th century,

double bookkeeping and Arabic numbers spread throughout the whole of Europe during the period of mercantilism and later throughout the world during the period of colonialism. With it also large

enterprises could be controlled effectively.

At the same time, the Roman numerals were replaced by the Arabic numerals in the decimal system. Because the double-entry bookkeeping with Roman numerals would not have worked and because without

the bookkeeping the use of Arabic numbers would not have been so necessary, both innovations have mutually reinforced each other.

Paccioli was a friend of Leonardo da Vinci and the method he described was brilliant as many Leonardo's ideas. It took into account the limited capacity of the human brain and was used for about

490 years without significant changes. But good methods will one day be replaced by better ones!

1.2. Industrialization

Industrialization demanded an extension of the method. In mercantilism, large trading houses with double-entry bookkeeping managed their businesses. The goods were transported over larger

distances and remained physically unchanged. Further processing took over smaller entrepreneurs. The double-entry bookkeeping was thus geared to the trade.

With industrialization and the emergence of larger factories, attention has shifted to adding value through a change in purchased goods and the use of labour and machinery. The bookkeeping was

supplemented by a cost accounting. The point here is to trace and evaluate the value added from the input (= cost element) to the output (= cost unit) via the processes running in the company (in

cost centers).

There were attempts to map cost accounting to accounts and thus to integrate them into the double-entry bookkeeping system. These attempts were again rejected as too laborious; or they could

never prevail in the companies. However, parts of these approaches have been included in the textbooks. Instead, the cost accounting was understood as a separate system and developed tabular as

an output of accounting. This led to a strict separation between external and internal accounting. It was only in the course of digitization that both systems became more closely linked again.

1.3. Regulation

In the course of modernity and the industrial age, accounting is becoming the focus of legislation and increasingly regulated. In 1794 this includes the introduction of the general accounting

requirement for companies with the General Prussian Land Law or in the French Code de Commerce of 1807, but also the emergence of the Prussian Commercial Code of 1861, converted into the German

Commercial Code in 1897 and still valid in its basics.

With the decree of the German and Prussian Minister of Economic Affairs and the German Commissioner for Pricing v. 11.11.37 - II 19263/37 VI 9991/37 concerning guidelines for the organization of

bookkeeping (as part of a single accounting system) in Ministerial Journal of Economy 1937 p. 239 and the decree of the German and Prussian Minister of Economic Affairs and the Reich Commissioner

for Pricing v. 16.1.39 - S 5151/39 VII - 50 - 49/39 general principles of cost accounting, external and internal accounting in Germany was heavily regulated. Although the regulations expired in

1953, they have greatly influenced companies in designing their accounting systems. Initially, business organizations in their respective industries took on the task of developing recommendations

for unified charts of accounts based on the Nazi revenue account framework, which has implemented the Process Allocation Principle. It was not until 1970 that the Federation of German Industries

developed the Industrial Accounts Framework (IKR) with the Annual-Accounts-Classification-Principle. In the 1980s, the tax consultancy company DATEV issued standard accounts and superseded the

recommendations of the associations. But they are more oriented to tax specifics and less to economically useful evaluations. The DATEV SKR03 follows the Process-Structure-Principle and SKR04 the

Annual-Accounts-Classification-Principle.

After 1953, only the regulations of the Commercial Code (HGB) and for corporations additionally the Law on Joint-Stock Companies (AktG) were obligatory, to which the Law on Companies with Limited

Liability (GmbHG) referred. As part of the 4th, 7th and 8th corporate law directives of the EC into German law, the rules of the AktG were adopted in 1985 in the 3rd book of the HGB and

reorganized the accounting. As part of the globalization of the capital markets from about the second half of the 1990s, international regulations gained in importance, which were significantly

influenced by the USA.

In 2003, the Council of the European Union approved a regulation requiring the application of the International Accounting Standards (IAS) (later: International Financial Reporting

Standards - IFRS) as of 2005 for consolidated financial statements of publicly traded companies. Within the framework of this development, Germany is breaking away from the accounting principles

previously codified in HGB and is primarily addressing Anglo-American accounting rules.

The HGB as well as the IFRS regulate the contents of the evaluations to be prepared and if necessary to be published and do not prescribe any concrete accounting technique. The double entry

bookkeeping can therefore also be replaced by another technique if it meets the quality requirements.

1.4. Digitalization

There is evidence that the emergence of accounting is closely related to the development of characters. Early records often deal with production and storage quantities of agricultural products.

Maybe the script was just invented to build an accounting department. It would not have been possible without a character.

Italian merchants developed the double-entry system in the 14th century. Government accounts of Genoa, dating from 1340, containing government receipts and expenditures, as well as all tax, bond,

and penalties, clearly show double entry bookkeeping. (Federal Association of Accountants and Controllers e.V., https://www.bvbc.de/baden-wuerttemberg/chronik/geschichte-der-buchhaltung /)

Indirect references to their existence are even dated to 1310. It uses the Arabic numbers instead of the Roman ones and also records every transaction twice, not just once, once on the debit side

and once on the credit side.

Luca Pacioli described this method in 1494 in a printed book as a Venetian bookkeeping - and spread it as a new standard from Italy throughout Europe. His book "Summa de arithmetica, geometria,

proportioni et proportionita", written in Latin, deals only with one chapter of the Venetian bookkeeping and otherwise deals with the system of Arabic numbers that reached Europe via the

commercial contacts of the Republic of Venice. For the first time since 1511, a record has been handed down from Germany using the double-entry method - by the accountant of the Fugger trading

house, Matthäus Schwarz. The Arabic numbers were comprehensively explained in German in 1524 with the book "Rechnung auff der Linihen und Federn" by Adam Ries (or Riese). In the 16th century,

double bookkeeping and Arabic numbers spread throughout the whole of Europe during the period of mercantilism and later throughout the world during the period of colonialism. With it also large

enterprises could be controlled effectively.

Digitalisation also shows a connection between accounting and technology. As with the development of characters and the introduction of Arabic numbers, the recording of business operations was

one of the first applications of EDP. For several hundred years accounting has been based on the manual transfer of numbers on paper, as has been the case for some 130 years. For about 30-40

years, companies have been using newer, computer-assisted procedures, which initially simulated the double-entry bookkeeping according to Paccioli only electronically. Initially, only individual

work steps were replaced by the machines, but then additional evaluations were created. On this basis, links and data transfers with non-accounting computer applications developed. For about 15

years, there has been a tendency to merge these applications and extend the focus on presenting the past as a database for the future. These techniques have not yet penetrated into the

textbooks.

These techniques are also treated as a trade secret of software providers. It is now time, as Pacioli 525 years ago with the Venetian accounting to describe today's possibilities as a stringent

system and thus replace the method of 1494 in the textbooks. At the same time, it can also be opened up to small companies who do not want to afford the expensive software and who lack the

specialist staff for their service. If a globally disseminated method is to be replaced, it must not only be usable in industrialized countries.

In the 21st century, there is a growing realization that organizational and technical knowledge is a fourth factor of production. This factor can also be increased easily. As in the nineteenth

century manpower was replaced by machinery, today the use of capital and labour can be reduced with a smarter organization and it can also conserve natural resources. For this, the processes and

sub-processes must first be analysed precisely and later simplified. The identification of the individual processes and sub-processes is necessary in order to constantly assess and improve them.

All conscious processes are planned more or less intensively and carried out according to this plan.

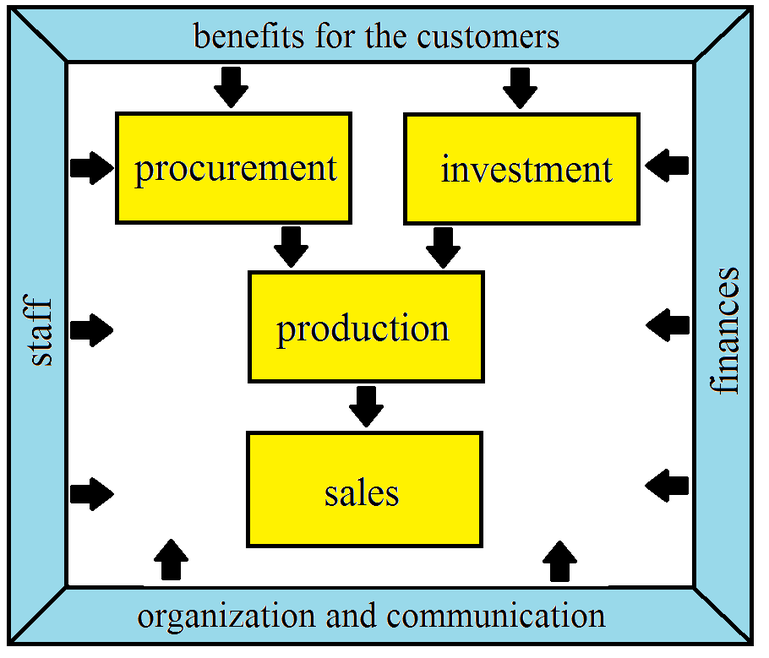

1.5. Value Added and Market

You can compare the companies with vehicles. There are trucks, tractors, vans, cars and motorcycles. There are also mobile machines in which locomotion is only a secondary purpose. On the other

hand, one can distinguish between production companies, trade and services. All vehicles have wheels, a chassis, an engine, a transmission and a steering. All businesses buy up inputs, create

value and sell their services. They combine capital goods, consumables and labor. As with the performance of a vehicle, there are major differences in operational performance, but also many

similarities.

The economic process is based on the production of a benefit for the customers of the company, which represents the operational purpose. The company sells this benefit if the proceeds of the sale

are greater than the cost of its production. Customers buy it if they value the benefit higher than the price the company demands. The production of benefits is limited by the capacities of the

companies. The customers have only a limited income available. They must prioritize and first buy the essential goods, then look for the maximum difference between utility and price. The

companies primarily produce the goods and services with the greatest difference between price and cost.

Fig. 1: Value creation process

Source: own representation

In the creation of value in business, a combination of the production factors capital and labour takes place. Specifically, the use of personnel and finances is coordinated. When using capital, a

distinction is made between potential factors and repeating factors. Potential factors arise from investments that determine the capacity of the operation. Repetitive factors are constantly

consumed in the company's added value and replaced again. The personnel deployment is predominantly attributable to the potential factors. The staff must first be recruited and often also trained

or trained. The potential also includes the professional experience of the employees. To a lesser extent, however, the workforce is also a potential factor if the employees work overtime and are

paid extra for it.

In addition to the potential and repetitive factors, the dispositive factor can also be identified, ie the ability to optimally organize and coordinate the processes. He creates a positive gap

between the selling prices and the unit costs and in the end generates the profits. The dispositive factor is mainly effective in selling the products. In a broader sense, this also includes

communication with the environment, with which a positive image of the company is built and maintained, which is a long-term prerequisite for the sale of one's own products.

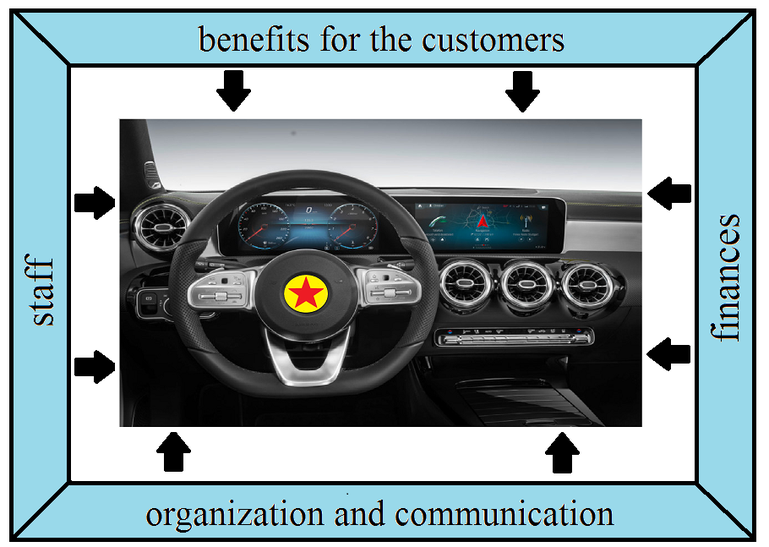

1.6. Navigation System of Business Management

The job of accounting is to support business management with data. It is similar to the cockpit of a car: the driver steers, but the instruments provide him with the data. There is a speedometer,

tachometer, fuel gauge and many indicator lights. This includes the cables that report the data from the different parts of the vehicle to the cockpit. The speedometer shows the current speed and

the driver decides whether he wants to maintain the speed, faster or slower drive. A big coach needs more ads than a small moped. But the moped driver must get the most important information. The

target group of this project are the moped riders, not the large corporations, but the small business owners!

As a data supplier and navigation system, accounting is of central importance in today's economy. If the driver cannot see anything, then an accident is very likely. Without an overview of the

economic situation and development, a company cannot be run safely.

Fig. 2: Navigation system

Source: own representation

The navigation system must be oriented to the needs of the specific company. Much can be taken from the experiences of others. These suggestions and templates will always have to be adjusted.

There is less need for adjustment when there are many templates for different industries, legal forms and company sizes from which to choose. Once this patterning solution has come a long way,

one day, as in clothing, almost everyone can find clothes that are comfortable with existing clothing, and at the same time select clothing from shapes and colours which the buyer looks good too.

1.7. Archiving

Archiving of business documents has always been understood as part of accounting. Thus, the German Commercial Code in § 257 (storage of documents, retention periods) and the tax code in § 147

(Ord-nungsvorschriften for the retention of documents) regulates this issue in connection with the accounting obligation. Archiving is thus part of the history of accounting; but this part is

still up to date.

Both for earlier entries on paper and in today's electronic data sets, doc-ument numbers indicating the process and a specific document are en-tered. To do this, systems have been made up of

letters that designate a document type and then numbers as a sequential number. Because the digits recommence each year, the year number is also widely used as part of the document number. When

digitizing the archives, each document can be saved as a separate graphic file. This makes it possible to limit an electronic transfer to the exact documents required. Then it makes sense to use

the file number for the file number. The following 26 document types can be identified, which can be distinguished in the Latin alphabet with one letter each.

Received invoices from suppliers (paid later)

Own or replacement document instead of received invoices from suppliers (paid later)

Generated invoices to customers (later paid)

Cash receipts received from suppliers (paid immediately in cash)

Own or replacement document instead of received cash vouchers from

suppliers (paid immediately in cash)

generated cash vouchers to customers (paid immediately in cash or by card)

Received card vouchers from suppliers (paid immediately by card)

Own or replacement document instead of received card documents from

suppliers (paid immediately by card)

Bank statements and credit card statements

(various banks included in the number)

Delivery notes and proof of service created for customers

Delivery notes and proof of performance received from suppliers

Own or replacement document instead of delivery notes and perfor-mance

certificates received from suppliers

Evidence of the removal of material or goods for own purposes

Contracts from which regular payments to suppliers follow

(without invoices or other documents)

Own or replacement receipt for regular payments to suppliers who are not contracted

Contracts that result in regular customer payments

(without invoices or other receipts)

Own or replacement receipt for regular payments from customers who are not

covered by contracts

insurance policies

other contracts

Logs (further subdivision in the document number)

Correspondence with customers (file name with customer number + date)

Correspondence with suppliers (file name with customer number + date)

other correspondence

to distinguish after sent + received, letter or e-mail

Organizational documents

own publications

Other storage / digitization

One could also combine parts of it and then differentiate in the document number, e.g. create the own and substitute documents, or other document types. If you want to create a more

differentiated system of document types, you can of course also use two letters.