deutsche Fassung

Version en español

Русская версия

Version française

5.1. concept

In the ERP systems of large companies, most internal and external accounting data is generated from the operational processes by data transfer. That should also be possible for small businesses.

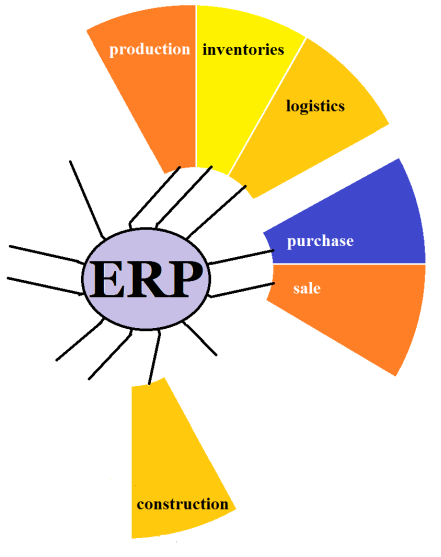

On the cover of this chapter, fig. 24 on page 97 has been pulled apart to symbolize ERP in small businesses without breaking the links. The capital letters behind the functions in Fig. 23 on page

96 identify software solutions which can cover this task, e.g. as modules in an ERP software:

A = Business Intelligence B = Production C =

inventories

D = logistics E = purchasing

F = sales

G = Personnel / HR H = Construction

I = Planning

J = investment and financing K = controlling L = accounting

There are 4 groups of modules:

1) Production, Supplies, Logistics, Construction, Purchasing and Sales:

They form the core of the operative activity and must be firmly anchored in the company. The modules production, logistics and design have to be very much geared to the industry and the specific

functions, while the stocks, purchasing and sales modules in the various industries are very similar. The parts of the ERP systems to be controlled by the small businesses are thus:

Fig. 30: ERP in small companies (internal)

(Source: own illustration)

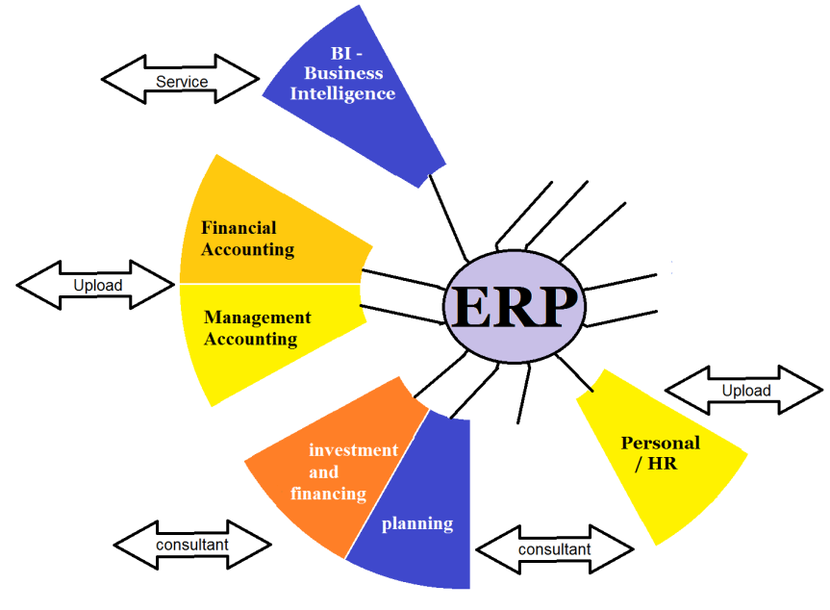

2) Accounting, Controlling and HR / HR:

They are standardizable. If the large companies get the data to be processed here from the group 1 of the modules by data transmission, then these data can be uploaded also over the Internet to

another computer. There, the data can be processed in client-capable programs. The evaluations to be created would be returned to the client in the same way. With automatically calculated key

figures, the management can be offered an aid to quickly recognize improvements and deteriorations in individual points.

3) Planning, investment and financing

The operational and strategic success and financial planning can be automated in technical terms. But there should be a coach, especially for the management of small companies, who asks the right

questions in this process. The right answers can then only be given out of the company. But it would not answer a question that is not asked. Therefore, the involvement of consultants in the

planning process would be highly recommended.

The same applies to large investment decisions. The computing technique for preparation can be automated, and the formulas can be easily applied using spreadsheets and free templates from the

Internet (e.g., from https: // mueller-consulting.jimdo.com/finanzen/investition/investitionsentscheidung/).

However, because of the long-term effects, the clarification of the facts is of central importance. Again, the right questions must be asked, which must be answered in the company.

The banks advise on financing decisions. However, they mainly want to sell their products. That's why companies also have to worry about independent information.

4) Business Intelligence

Business Intelligence (BI) basically describes a set of methods for obtaining business-relevant data. First use in the management found IT systems already in the 1960-ies in the form of

management information systems (MIS). Small companies need the support of experts who can professionally and mechanically evaluate the data generated in modules B to L. The provider of such

services could also take care of the entire information technology.

The externally covered parts of the ERP system of small businesses are thus:

Fig. 31: ERP in small businesses (external)

(Source: own illustration)

In Fig. 10 on page 65, the triangular logic of posting records was addressed. In section 3.6. The mathematical derivation of cash flows from the accounting data, from which balance sheets and

profit and loss accounts are prepared, was dealt with. Data collection by small businesses will be closer to cash flows. The development of a small business concept should therefore examine

whether the reverse approach can be used to derive data for the profit and loss account from cash flow and balance sheet data.