deutsche Fassung

Version en español

Русская версия

Version française

5.3. Data acquisition and data transmission

5.3.1. annual financial positions

The data collection regarding profit and loss account as well as cost type accounting overlaps. It's almost the same data, only processed differently. We will first ask for the data from the

balance sheet, income statement and cash flow statement. Data collection is rarely done in the accounting department. It is common practice to collect the information accumulated in various

places in the day-to-day tasks and to transfer it via interface to the accounting software. The structures presented in sections 5.2.1-3 can be summarized as follows:

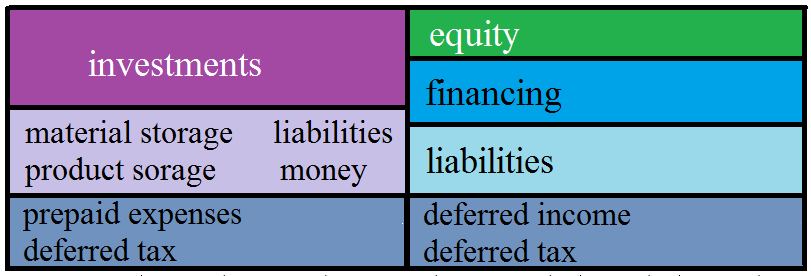

Fig. 45: Financial Statements

(Source: own illustration)

Neutral income and expenses, other assets and other liabilities have not been included in the figure for the sake of simplicity.

The data from the value chain of goods purchasing - material storage - production - product storage - goods issue is available without gaps in those parts of the ERP system that can not be

outsourced from the company (see Fig. 30 on page 175). With them, the day-to-day business is handled and these data are up-to-date and complete because of the motive for earning money. The

information can also be generated with a spreadsheet and transmitted via an interface. Section 3.3 details this path. In a research project in the winter semester 2014/15, the author simulated a

fictitious company in multi-client financial accounting software in which all accounting data was imported from spreadsheet files via an interface.

Fig. 46: ERP modules and value chain

(Source: own illustration)

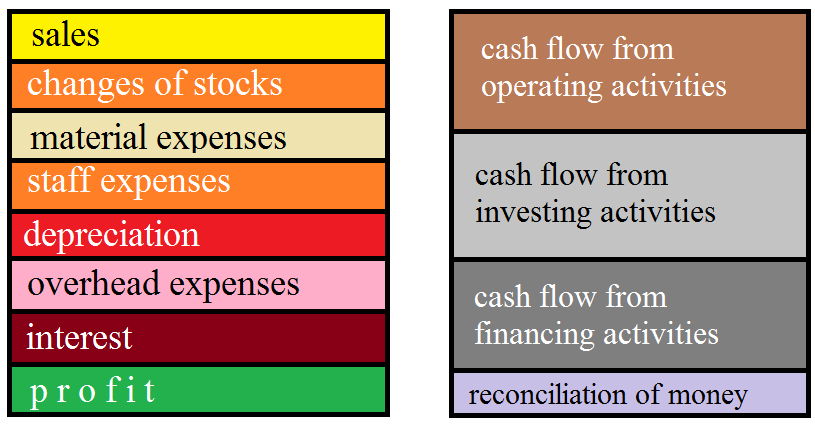

This value chain results in the data of some balance sheet and income statement items. All withdrawals from the material storage trigger the posting record "debit Material Expense, credit

Inventories". The completion of products is recorded using the posting record "debit inventories, credit inventory changes". The sale and delivery of products is accounted for by the changes in

inventories and sales receivables. This is shown in the following figure.

Fig. 47: Value chain and final positions

(Source: own illustration)

This value-added process causes deposits from the receivables. For the purchases of the material, the labor and other goods but also payments are effected. Purchases of goods, capital goods and

overheads are initially recorded as a liability and then the incoming invoices are paid. Investments lead to depreciation and their financing is paid and repaid. The same posting record can be

stored for all similar transactions.

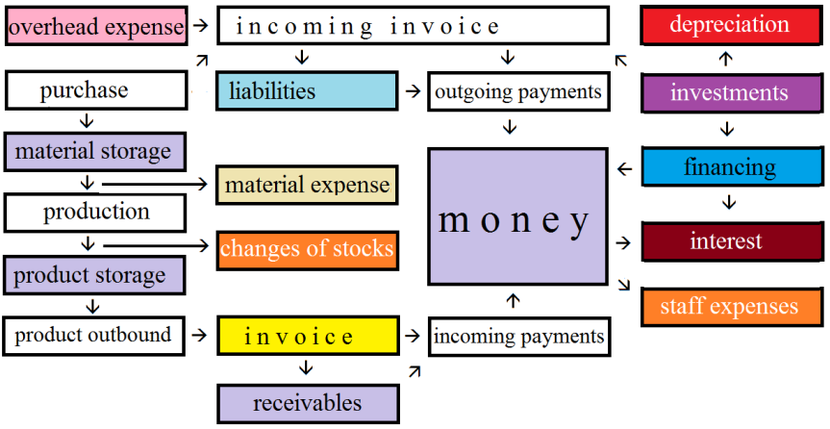

There is a goods-money cycle that can be described with the following figure:

Fig. 48: Goods-money cycle and closing positions

(Source: own illustration)

With the depreciation, interest and personnel expenses, the rectangles on the right contain the items that were previously missing in the income statement according to Fig. 45 on page 198. Your

data does not arise directly from the value creation process. The balance sheet items, with the exception of equity, deferred income and deferred taxes, which can be measured at the end of the

preparation of the annual financial statements, are also complete. The rectangles at the right end of the figure result from investment controlling, payroll and a finance database, which are

present in modules of the ERP system that are externally managed and updated by data that the entrepreneur has in them Upload modules.

Fig. 49: ERP system and closing items

(Source: own illustration)

For personnel and salary payments, professional solutions should be sought from specialized providers. The data for the hours worked can be recorded by the entrepreneur himself and transmitted

electronically. For investment and depreciation, investment controlling can provide the necessary data. Just as there is a depreciation plan for investments, there is a repayment plan for

financing, from which the interest and repayment installments can be automatically transferred to accounting records.

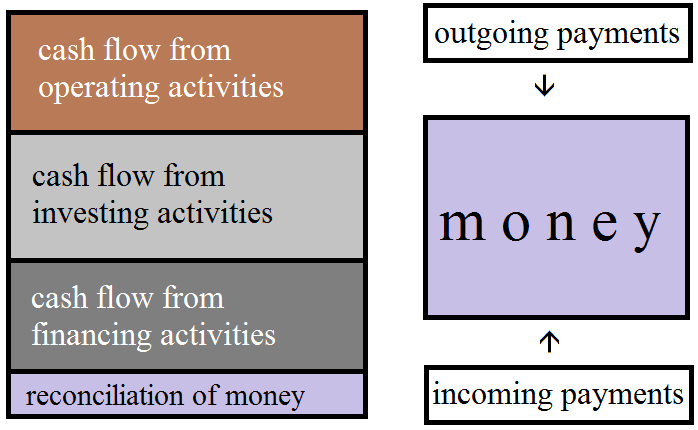

It has already been shown in section 3.6 that the cash flows can be calculated derivatively from accounting with the cumulative offsetting postings. However, they can also be generated originally

from the data of electronic banking. This can be particularly important for a very short-term consideration, if not wait until the booking of all business transactions. Then, links between the

cash flow statement items and the bank account transactions must be established.

Fig. 50: Cash flow and payment transactions

(Source: own illustration)

Thus, e.g. Incoming payments with indication of a customer no. or bill no. Deposits from customers. Sales of fixed assets would have to be adjusted. Self-generated payments can be assigned to the

flows for "to suppliers" and "for employees" using the offsetting entries for the import into the booking. With regard to investment activity, it is assumed on a simplified basis that the

investments made were paid. Unpaid invoices are allocated to operational activities. Tax payments are also initiated and are also assigned to the tax codes via the counter accounts. Not

automatically defined:

Cash flow from operating activities

5. + other deposits, other than investment or financing activities

6. – other payments, other than investment or financing activi-ties

Cash flow from investing activities

7. + Deposits due to financial investments in the

context of short-term financial management

8. – Disbursements due to financial investments in the

context of short-term financial management

9. + Interest received

10. + Dividends received

Cash flow from financing activities

1. Deposits from equity contributions

2. + Deposits from issuing bonds and raising (financial) loans

4. + Deposits from grants / grants received

6. – Paid dividends

If there are payment transactions that are not automatically assigned according to the criteria mentioned in electronic banking, a manual assignment would probably be made to one of these

items.

Thus, the following rectangles are still open from Fig. 45 on page 198 and 48 on page 202:

Fig. 51: remaining items

(Source: own illustration)

Equity, prepaid expenses and deferred taxes result from the preparation of quarterly and annual financial statements. For the capture of incoming invoices, an invoice receipt file must be

created. The processes generated from the purchase of goods are to be read in there. Invoices from overheads that were not included in the purchase of goods should be added.

5.3.2. cost accounting positions

For cost accounting, it is necessary to enter the account that controls the cost element as well as the cost center and, if necessary, the cost object. In Fig. 41 on page 194, the possibility of

a combination of cost center and cost unit no. treated. For the entry of this additional information, there are the following case groups:

material withdrawal

With the article no. of the material that is also required for the stock update, the expense account would be defined. At cost centers here only the production with the cost centers 30 to 69

comes into consideration, if one considers the revised BDI proposal from Fig. 40 on page 191 ff.; or cost center 24 for research and development consumption. The worker who removes the material

would know which cost center he belongs to. The last three digits of the cost center no. would be for the cost unit, which is currently being worked on. Automated capture could be organized with

bar code readers.

Payroll and billing

In payroll accounting, employees would be assigned to a cost center to which wages and salaries would be automatically posted. In addition, a quantity recording of the hours worked should be

organized, which defines the fulfilled tasks more closely. It would also be recorded if one employee helped out in another cost center. Likewise, the individual wage costs would be recorded for

the working hours that would be worked directly on the cost unit. The transfers would be made via separate G / L accounts; the bookings would cancel each other out. Only the cost center transfer

would remain. In the case of direct costs, "debit production wages, credit overhead costs" would be posted. Quantity entry could be done in spreadsheet. The file could also generate the record

for the transfers via a flexible interface.

invoices

Incoming invoices can relate to material purchases, investments and material expenses. For material purchases, the cost center and cost unit would only be known if it were purchased directly for

a specific order. Otherwise, the definition would be made only with the material removal. In order to avoid coverage gaps, the cost center would initially use 10000 lt. Of revised BDI proposal

(Fig. 40 on page 191 ff.), Which would then also be addressed in the offsetting entry of material withdrawal. For investments, a cost center and possibly also a cost center would be entered so

that the depreciation from investment controlling (asset accounting) can later be assigned to the right cost center.

For all invoices should immediately a record with assignment of a bill no. and recording the vendor no., amount and due date are generated in an invoice receipt file. The substantive examination

would be carried out afterwards; Account and cost centers can be added. A variable interface transfer file can be created from a spreadsheet file to account for material purchases, investments,

and overhead. For the payment the electronic banking function of the accounting program (module in the ERP system) would be used.

cash purchases

Cash purchases are comparable to invoices, except that no payment has to be made. The factual accuracy was already checked by the initiator with the payment and he would have to know the facts

for the definition of account and cost center. In contrast to the past, cash receipts can be paid with a credit card or bank card. The file of the spreadsheet with which the cash book is kept

must therefore distinguish these 3 possibilities. Otherwise, the procedure is the same as for incoming invoices. One could also organize that the cash bookings are attached to the transfer file

of the incoming invoices.

regular payments

There are other expenses for which contracts exist but no invoices. For example, rents, magazine subscriptions, insurance policies or contributions to associations are recorded on the basis of

the payments. For the update, a file should be maintained with these expenses, in addition to the amounts with due dates and the account and cost center definition is stored. During payment, this

prepared data record can then be transferred to the records to be posted by "copy-and-paste". It could also be arranged that the bookings for regular payments be attached to the transfer file of

the incoming invoices.

imputed costs

imputed costs are recognized in addition to the expenses. But also the accounting department must be used, because the cost type is over the account number. controlled. Therefore, a separate

account area must be created, in which the booking and offsetting entries cancel each other out. To avoid error messages, they can then be pro forma assigned to a balance sheet item with little

movement (for example, in equity).

For imputed costs, a distinction is made between additional costs and other costs. Other costs change expenses, while there are no additional costs for additional costs. Practically, however,

both subspecies are processed the same, except that the corresponding effort in the other costs treated as neutral effort and with a cost type no. between 9000 and 9999 (see Fig. 39 on page 189

ff.) is passed on to cost accounting. Despite the credit balance, the clearing account for the offsetting postings is also part of the neutral expenses.

The usual imputed cost types are:

imputed interest:

Other costs to take account of the capital tied up by the cost centers instead of bank rates in general cost centers.

imputed depreciation:

Other costs for consideration of replacement costs and a different useful life compared to tax depreciation.

imputed rents:

Other costs compared to space costs to take account of lost profits from an alternative use of space (rent instead of use).

imputed entrepreneurial wage:

Additional costs to take into account the labor of the co-entrepreneurs.

imputed risks:

Additional costs to take into account calculable risks - at the same time other costs compared to expenses of an unusual amount, which is deferred as a neutral expense when the risk occurs.

For settlement, the imputed costs are calculated once and updated at longer intervals. It is a good idea to include them in the file for regular payments, to define the dummy account and the cost

center there, and then execute them once a month.

5.3.3. quarterly and annual financial statements

After ensuring that all facts and documents of the quarter or year to be closed have been recorded, there are some additional tasks. These transactions are then recorded in the 13th period so as

not to distort the data of the regular business activity. It is a matter of:

depreciation

Property, plant and equipment and intangible assets are depreciated. They are already recorded monthly. Because tax depreciation is an annual amount, depreciation has to be recalculated on an

annualized basis. The monthly depreciations in periods 01 to 12 are then adjusted in period 13. These operations can automate asset accounting. It only needs to be checked if the items are still

there. If there were indications that the current value of fixed assets could be lower than the book value, unscheduled depreciation would also have to be examined.

stocktaking

Inventories should be checked once a year to see if stocks are really there. Deviations have to be corrected. At the balance sheet date - the deadline can also be brought forward - the deviation

would be a process of the 13th period. However, there is also the alternative of permanent inventory, where the check is distributed throughout the year and part of the inventory is checked every

month or every week. Then the adaptation would be a process of the current period.

When checking, it must also be considered whether the condition of the goods is still flawless or impaired. In a further step, the book values would have to be compared with current prices in

order to determine whether there could be an economic impairment. Inventory inventory checks include templates that allow you to calculate the corrective entries in the spreadsheet and to create

the adjustment postings via an interface.

years delimitation

Accruals are not to be equated with accrual items in the balance sheet. It concerns all processes, where the achievement is effected not at times, but in periods. If the periods of the services

do not coincide with the financial year, they must be delimited. With the typical settlement (first the achievement, then the money), the demarcation takes place over the demands and liabilities.

Only in the atypical settlement with prepayment a deferred entry must be formed. In practice, it will always be about the same facts, which then only need to be updated. For calculating the time

distribution and the amounts, there are also spreadsheet tools with which the adjustment postings can be created.

update of provisions

Provisions are uncertain liabilities that are often estimated in amount. When updating the accruals, you determine which transactions have been further clarified or settled since the last update.

If the liability has been fully or partially fulfilled, it is called the consumption of the provision. For this, the expense is offset by the provision (= minus expense). If, according to recent

findings, there is no obligation, the provision is to be released. This creates a yield. It is also necessary to check whether new risks are identifiable, for which additional provisions need to

be posted to the provision. Provisions for calculation and posting are also available for the provisions.

tax calculation

Based on the profit and loss account and possible adjustments to the taxable profit determination (for example non-eligible expenses), the tax assessment for the financial year can be simulated.

However, the tax return can be submitted later. The tax to be paid can then only be posted as a tax provision.

In addition, the tax provisions of the last due date must be updated. Tax payments have their offsetting entries in the tax provision. For incoming tax assessments, it must also be checked

whether these correspond to the simulation of the last financial statements. Also for the tax calculation there are templates for the spreadsheet.

5.3.4. Technology of data transmission

The mass of data for the current business transactions, the cost accounting and the final work can be generated with the spreadsheet and imported into an accounting software as part of an ERP

system. The data collection then gets a strong similarity to the simple accounting, which is described in section 2.9.1. was addressed. If a service provider offers accounting in a multi-tenant

software, the data collected in journals can be uploaded there and at the same time be a double entry bookkeeping.